Originating from the vision of children, the Tuusula-based Martta Wendelin Daycare Centre embodies respect for children and sustainable development.

Since the summer of 2022, this exceptional building has added life to the scenery of the municipality of Tuusula in Southern Finland. The Martta Wendelin Daycare Centre, designed with children’s needs in mind, won the prestigious Finlandia Prize for Architecture for its distinctive architecture and execution.

User-oriented approach and ecological values steered the project

As part of the service network design in 2018, Tuusula resolved to replace several old daycare centres with new buildings. Stemming from a vision of preschoolers, the Martta Wendelin Daycare Centre was established, resulting in a new daycare centre in Tuusula with 10 groups, providing about 200 daycare places for children.

“The idea for the daycare centre was born when we started sketching a vision of the dream playground together with preschool-aged children. Later, the Martta Wendelin Society joined the project. This was natural, as the artist Martta Wendelin, known for her depictions of Finnish rural and home life, spent most of her life right here in Tuusula,” recalls Tiina Simons, Director of Education in Tuusula, about the early stages of the project.

Martta Wendelin’s art is also a prominent part of the daycare’s interior decoration.

“The entire project has been carried out using user-centred design. The history of Tuusula has been brought into the building in a skillful and beautiful manner,” says Pirjo Sirén, Director of Municipal Development.

Significant efforts have been made in the implementation of the Martta Wendelin Daycare to utilise environmentally friendly solutions and climate-smart construction. This can be seen, for example, in the energy efficiency and in the way the principles of the circular economy have been taken into account both during the construction phase and in the planning of the building’s life cycle.

Thanks to its environmental friendliness, the project has been financed with green finance from MuniFin.

“Although the high-quality implementation of the daycare required a significant investment, we expect to achieve savings on the operating budget side. Combining four early education units into one makes the organization of operations more cost-effective and the maintenance of the property easier,” says Markku Vehmas, the acting Chief of Staff of the municipality.

Children and nature come first

The Martta Wendelin Daycare Centre embodies respect for the environment and sustainable development. The building has been constructed with materials that prioritise environmental friendliness and health.

“The structures of the exterior and interior walls as well as the intermediate floors have used CLT massive construction that acts as a carbon sink. The design of the spaces has focused on diversity and flexibility so that they can serve different purposes. The yard designed for play and exercise beautifully opens to the south. Part of the forest has also been left on the yard area to be preserved, as well as a stormwater puddle where children can jump to their heart’s content in rainy weather,” Sirén describes.

“The building has also not been filled with colors or artworks. The wooden surfaces create frames into which the children can bring colors,” Simons continues.

The exceptional nature of the building has brought various recognitions to the municipality. In addition to the Finlandia Prize for Architecture, the daycare centre has also won the 2023 International Award for Wood Architecture, awarded by five European architectural journals.

“I also consider the awards as a tribute to our high-quality early childhood education,” Simons states.

Most importantly, positive feedback has been received from the users of the building.

“We have received particular praise for the brightness and spaciousness of the spaces. Children love being at the daycare and enjoy themselves both indoors and in the yard activities,” Simons rejoices.

Finance for Finland's green transition

MuniFin has offered its customers green finance for sustainable investments since 2016. Funding for green projects is sourced by issuing green bonds. For investors, MuniFin’s green bonds offer a way to finance positive impacts through carefully selected projects in e.g. buildings, transportation and renewable energy categories.

MuniFin’s inaugural NOK social bond was issued on 13 February. Despite ample supply from SSA issuers in the NOK market, the demand for the NOK 2 billion issue was strong, with a high quality investor base.

The issue marked both MuniFin’s first ESG labelled bond and the first NOK trade this year. The books built very quickly and were closed at a spread of +25 bps over 3-month Nibor.

“Over the past years, MuniFin has established themselves as a frequent issuer in the Nordic market, popular amongst a wide array of investors. The new issue marks the first social bond issued by MuniFin in Norway and the label was a significant contributor to the great investor demand”, says Hedda Giæver, Head of IG International, DBN Bank ASA.

The strong investor base showcased significant interest from bank treasuries, as well as domestic and foreign real money, including pension insurance and asset managers.

80% of the issue was allocated to Norwegian investors.

“We are extremely happy to have been able to return to the Norwegian Krona market. What’s even more pleasing is to be able to do it with a social bond. It is in the very core of our Sustainability Agenda to provide financing to social projects and increase their share in our lending portfolio. We are ever grateful for the support from our investors”, says Aaro Koski, MuniFin’s Funding Analyst.

Transaction details

Issuer:

Municipality Finance (KUNTA, MuniFin)

Issue Rating:

Aa1/AA+

Status:

Senior unsecured

Reoffer Price:

99.631% / 4.083%

Reoffer Spread:

3mN+25bps

Issue Size:

NOK 2bn

Settlement:

20 February 2024

Maturity:

20 February 2029

Coupon:

4% Fixed, Annual, Act/Act Icma Unadjusted Following

Listing:

Nasdaq Helsinki

ISIN:

XS2769883955

Lead Manager:

DNB Markets

Further information

Joakim Holmström, Executive Vice President, Capital Markets and Sustainability, +358 50 4443 638 Antti Kontio, Head of Funding and Sustainability, +358 50 3700 285 Karoliina Kajova, Senior Manager, Funding, +358 50 5767 707 Lari Toppinen, Senior Analyst, Funding, +358 50 4079 300 Aaro Koski, Analyst, Funding, +358 45 138 746

The Group’s net operating profit excluding unrealised fair value changes in January–December increased by 3.2% and amounted to EUR 176 million (EUR 170 million). The net interest income grew by 7.5% propelled by rising short-term market rates and totalled EUR 259 million (EUR 241 million). The growth in result was slowed down by an increase in costs.

Net operating profit amounted to EUR 139 million (EUR 215 million). Unrealised fair value changes amounted to EUR -37 million (EUR 45 million) in the financial year. Unrealised fair value changes were influenced in particular by changes in interest rate expectations and credit risk spreads in the Group’s main funding markets.

Costs in the financial year amounted to EUR 82 million (EUR 73 million). The growth in costs was primarily driven by the almost quadrupled guarantee commission of EUR 13 million (EUR 4 million) paid to the Municipal Guarantee Board, which resulted from a change in the calculation method. The guarantee commission is a compensation for the guarantees the Municipal Guarantee Board grants to MuniFin’s funding.

The Group’s leverage ratio continued to strengthen, standing at 12.0% (11.6%) at the end of December.

At the end of December, the Group’s CET1 capital ratio was very strong at 103,4% (97.6%). CET1 capital ratio was well over the total requirement of 13.9%, with capital buffers accounted for. Because MuniFin Group only has CET1 capital, Tier 1 and total capital ratios are the same with the CET1 capital ratio, 103.4% (97.6%).

The Russian invasion of Ukraine has not had a significant effect on the Group’s operations. The war has accelerated inflation and pushed up market interest rates, which has had a positive effect on the Group’s net interest income, but also increased costs. Because of the geopolitical uncertainty caused by the war, the Group has maintained strong liquidity buffers. Otherwise, the war has had only a minor effect on the Group’s operations.

Long-term customer financing (long-term loans and leased assets) excluding unrealised fair value changes totalled EUR 32,948 million (EUR 30,660 million) at the end of December and saw an increase of 7.5% (5.5%). New long-term customer financing in January–December was at the same level as in the previous year and amounted to EUR 4,370 million (EUR 4,375 million). Short-term customer financing totalled EUR 1,575 million (EUR 1,457 million).

Of all long-term customer financing, the amount of green finance aimed at environmentally sustainable investments totalled EUR 4,795 million (EUR 3,251 million) and the amount of social finance aimed at investments promoting equality and communality totalled EUR 2,234 million (EUR 1,734 million) at the end of December. The total amount of this financing increased by 41.0% (42.9%) from the previous year. The ratio of green and social finance to long-term customer financing excluding unrealised fair value changes grew by 5.1 percentage points to 21.3%. In late 2023, the Group published its sustainability agenda, which extends to the year 2035. By the end of 2030, the Group’s goal is to increase the share of green and social financing to one third of all long-term customer financing, and by the end of 2035 reduce emissions from financed properties by 38% from the 2022 level.

In 2023, new long-term funding reached EUR 10,087 million (EUR 8,827 million). At the end of December, the total funding was EUR 43,320 million (EUR 40,210 million), of which long-term funding made up EUR 39,332 million (EUR 35,560 million). In March and in June 2023, the Group decided to repay the debt related to the European Central Bank’s targeted longer-term refinancing operations (TLTROIII). The debt totalled EUR 2,000 million.

The Group’s total liquidity remained very strong, standing at EUR 11,633 million (EUR 11,506 million) at the end of the financial year. The liquidity coverage ratio (LCR) stood at 409% (257%) and the net stable funding ratio (NSFR) at 124% (120%) at the end of the year.

The Board of Directors proposes to the Annual General Meeting to be held in spring 2024 a dividend of EUR 1.69 per share, totalling EUR 66.0 million. The total dividend payment in 2023 was EUR 1.73 per share, totalling EUR 67.6 million.

Outlook for 2024: The Group expects its net operating profit excluding unrealised fair value changes to be at the same level or higher than in 2023. The Group expects its capital adequacy ratio and leverage ratio to remain strong. The valuation principles set in the IFRS framework may cause significant but temporary unrealised fair value changes, some of which increase the volatility of net operating profit and make it more difficult to estimate. A more detailed outlook is presented in the section Outlook for 2024.

Comparison figures deriving from the income statement and figures describing the change during the reporting period are based on figures reported for the corresponding period in 2022. Comparison figures deriving from the balance sheet and other cross-sectional items are based on the figures of 31 December 2022 unless otherwise stated.

Key figures

Jan–Dec 2023

Jan–Dec 2022

Change, %

Net operating profit excluding unrealised fair value changes (EUR million)*

176

170

3.2

Net operating profit (EUR million)*

139

215

-35.5

Net interest income (EUR million)*

259

241

7.5

New long-term customer financing (EUR million)*

4,370

4,375

-0.1

New long-term funding (EUR million)*

10,087

8,827

14.3

Cost-to-income ratio, %*

32.4

23.9

35.7

Return on equity (ROE), %*

6.6

9.9

-33.5

31 Dec 2023

31 Dec 2022

Change, %

Long-term customer financing (EUR million)*

32,022

29,144

9.9

Balance sheet total (EUR million)

49,736

47,736

4.2

CET1 capital (EUR million)

1,550

1,482

4.6

Tier 1 capital (EUR million)

1,550

1,482

4.6

Total own funds (EUR million)

1,550

1,482

4.6

CET1 capital ratio, %

103.4

97.6

5.9

Tier 1 capital ratio, %

103.4

97.6

5.9

Total capital ratio, %

103.4

97.6

5.9

Leverage ratio, %

12.01

11.6

3.8

Personnel

185

175

5.7

* Alternative performance measure. All figures presented in the Financial Statements Bulletin are those of MuniFin Group, unless otherwise stated

Comment on the 2023 financial year by President and CEO Esa Kallio

The year 2023 was the fourth consecutive year marked by instability. The rising geopolitical tensions and market volatility did not significantly affect MuniFin’s performance, and we were able to successfully carry out our core mandate of ensuring the availability of affordable long-term financing for our customers.

In 2023, the inflation exacerbated by the Russian invasion of Ukraine in 2022 took a downward turn, and interest rate hikes tapered off. Geopolitical tensions increased across the world throughout the year, and expectations of central bank measures caused uncertainty in the capital markets.

In Finland, the first half of the year was characterised by the parliamentary elections held in April and the ensuing government formation talks that stretched into June. The new government programme is unlikely to affect municipal operations directly. In the housing sector, our customers have been concerned about the government programme’s entries concerning right-of-occupancy housing and state-subsidised housing production. In this uncertain operating environment, our role as our customers’ trusted partner has grown even more important.

The demand for financing from our customers in the municipality sector was quiet at the beginning of the year, but demand picked up towards the end of the year close to the previous year’s level. Temporary tax benefits boosted municipal finances, causing municipalities to have lower financing needs. In municipal finances, 2023 was still a relatively good year, but started to weaken at the end of the year.

In the affordable social housing sector, financing needs were higher than in the year before. Our housing sector customers have suffered from rising construction costs for several years now, which has decreased the start of new building contracts. Rising interest expenses have taken a further toll on them since 2022. Towards the end of the year, however, the demand for financing started to pick up as construction costs levelled off and right-of-occupancy project starts were rushed because of the new government programme’s entries.

The new wellbeing services counties started their operations on 1 January 2023, and we financed the wellbeing services counties within the limits set by the Municipal Guarantee Board (MGB). The EUR 400 million limit for long-term finance set by the MGB was reached before the end of the year, and we could no longer fulfil wellbeing services counties’ financing requests for 2023 after that.

Our funding operations were a success despite the fluctuation in the capital markets. Our issuances were well-timed, and all our transactions were successful. We continued to keep our liquidity at a strong level throughout the year to ensure the availability of financing for our customers in all conditions.

Our operations continued in the usual manner in 2023, and our profitability was slightly higher than in 2022.

In 2023, we revised our strategy to further underline our core mandate. Our revised strategy highlights sustainability and our role as an enabler of sustainable welfare in society. We also made efforts to better assess and measure the impact of our operations. In October, we published our sustainability agenda, which sets the framework and goals for our long-term sustainability work. The agenda focuses on our business operations, i.e. the products and services offered to our customers, and the long-term impact achieved through them.

Outlook for 2024

The global economy is starting 2024 in a weakening economic cycle. The demand-slowing effects of interest rate hikes are reaching their peak and making sources of growth scarce, while fiscal policies are contracting as governments need to curb their debt. The geopolitical environment continues to remain unpredictable. On the upside, the cooling economy is helping to cushion cost pressures, and inflation is falling towards the ECB’s target of 2% in the euro area. The ECB is expected to commence interest rate cuts in 2024.

In Finland, the combined effect of factors saddling growth will peak in the first half of 2024. As the months pass and inflation eases, consumer purchasing power increases and interest rates start to come down moderately, the domestic market will gradually kick off economic recovery. Towards the end of the year, the export market may also start to contribute to recovery. Because of the low starting level, Finland’s GDP growth may nevertheless remain slightly in the negative in 2024.

The economic downturn will inevitably reflect on employment. In many sectors, Finland is suffering from such high structural labour shortages that strong growth in unemployment seems unlikely, but the employment outlook is nevertheless looking risky. It remains difficult to estimate how severe the construction sector’s recession will become and what multiplier effects this will have in other sectors. The euro area’s inflation trajectory is also looking somewhat uncertain. If inflation proves more persistent than anticipated and expected interest rate cuts are postponed, the downturn may drag on and push unemployment up more than expected.

Although Finland’s government programme sports ambitious fiscal efforts, public finances are projected to continue to show a significant deficit and high levels of debt in the coming years. The higher-than-expected increase in health and social services expenditure and financing costs and the cyclical decrease in tax income are making public finances difficult to balance. After a few exceptionally strong years, the municipal sector will return into serious deficit as various positive non-recurring items cancel out, costs increase and central government transfers decrease. The main uncertainties in municipal finances stem from the general economic development, the upcoming changes to central government transfers and the potential additional costs arising from the transfer of employment and economic development services (TE services) to municipalities.

Considering the above-mentioned circumstances, the Group expects its net operating profit excluding unrealised fair value changes to be at the same level as or higher than in 2023. The Group expects its capital adequacy ratio and leverage ratio to remain strong. The valuation principles set in the IFRS framework may cause significant but temporary unrealised fair value changes, some of which increase the volatility of net operating profit and make it more difficult to estimate.

These estimates are based on a current assessment of the development of MuniFin Group’s operations and the operating environment.

Municipality Finance Plc

Further information:

Esa Kallio, President and CEO, tel. +358 50 337 7953 Harri Luhtala, Executive Vice President, Finance, CFO, tel. +358 50 592 9454

Download the full Financial Statements Bulletin 1 January–31 December 2023

MuniFin’s annual report 2023 will be published around 7 March 2024. On the same date, MuniFin Groupwill also publish the Pillar III disclosure based on the Capital Requirements Regulation, and the Corporate Governance Statement.

Only two weeks after MuniFin’s highly successful opening transaction of the year, MuniFin priced a new USD 1.5 billion benchmark on 24 January. Investor demand was phenomenal from the beginning and resulted in an all-time record orderbook of USD 4.4 billion. The bond is also the largest USD issuance since 2021.

The record-breaking bond carries a coupon of 4.250%, and was priced at SOFR mid-swaps+47bps, equivalent to a spread of +22.6bps over the UST 3.75% due 31 December 2028. From the initial price thoughts of +50bps, MuniFin was able to tighten the final pricing by 3bps due to the outstanding demand from high-quality investors.

The final orderbook was of very high-quality and geographically diverse with 83 investors participating. In terms of investor type, the majority of allocations went to banks (49.1%), followed by central banks and other official Institutions (39.5%) and Fund Managers (11.4%).

Considering the busy primary market, the result was quite impressive and received praising comments from the joint lead managers on the transaction.

“Congratulations to the MuniFin team on their first USD benchmark outing of 2024. The new USD 1.5 billion, 5-year benchmark garnered a high-quality orderbook amidst a busy primary market for SSA issuers. MuniFin’s agility in adapting to market windows once again enabled them to achieve attractive cost of funding for their activities which support the mission of building a better and more sustainable future for its clients. Deutsche Bank is proud to have been involved in this transaction”, said Katrin Wehle, Managing Director and Head of SSA CDM Origination at Deutche Bank.

MuniFin’s funding programme is progressing at a very good pace, as after this transaction, the company has printed nearly 25% of its EUR 9–10 billion programme for 2024.

“It has been a busy start for us at MuniFin, as we decided to kick off our funding year with two benchmarks and printed already a quarter of our funding programme within less than one month. We are extremely excited to break a new record with an overwhelming demand of USD 4.4 billion for this USD benchmark. We are humble for the exceptional reception and want to extend our thanks to all our investors and joint lead managers who participated in making this happen”, says Senior Manager KaroliinaKajova from MuniFin’s funding and sustainability team.

Transaction details

Issuer

Municipality Finance Plc (“MuniFin”)

Issue Amount

USD 1.5 billion

Issuer Rating

Aa1 /AA+ (Moody’s / S&P) (all stable)

Pricing Date

24 January 2024

Settlement Date

31 January 2024 (T+5)

Maturity Date

31 January 2029

Re-offer Price /Yield

99.942% / 4.263%

Annual Coupon

4.250%

Re-offer Spread

Mid-swaps +47bps

Spread vs Benchmark

UST 3.750% due 31st December 2028 +22.6bps

Listing

Helsinki Stock Exchange (Regulated market)

Documentation

Issuer’s Debt Issuance Programme dated 7 September 2023

ISIN

XS2757519280 / US62630CEK36

Joint Lead Managers

Barclays, BMO, Citigroup, Deutsche Bank

Comments from joint lead managers

“Congratulations to the MuniFin team for another fantastic outing in the USD benchmark space. We are delighted to see the team achieve a record orderbook well in excess of USD 4bn and with granular interest from over 80 investors. The USD 1.5bn 5Y deal priced with minimal concession to the secondary curve, testament to the strong name recognition that MuniFin enjoys with investors around the world.“

Massimo Antonelli, Managing Director BMO Capital Markets

“Congratulations to the MuniFin team for a phenomenally successful USD outing, with this latest benchmark extending the issuer’s USD curve. The largest ever USD orderbook for MuniFin at USD 4.4 billion, as well as its joint-largest USD print over the past decade at USD 1.5 billion, is a testament to the firm standing of MuniFin amongst the global investor community. Moreover, size did not come at the expense of price, with the trade seeing a 3bps move tighter in spread during execution and crucially with no attrition in the size of demand. Barclays is honoured to have supported this transaction.”

Francesco Polon, Director, SSA Debt Capital Markets, Barclays

“An resounding return to the US dollar market for MuniFin. With a constructive and supportive primary market and stable macro backdrop, MuniFin priced their largest transaction in dollars since 2021 and achieved its largest ever orderbook with the transaction 2.9x oversubscribed. Citi is delighted to have been involved in this record-breaking trade. Congratulations!”

Ebba Wexler, Managing Director, Head of SSA DCM, Citi

Further information

Joakim Holmström, Executive Vice President, Capital Markets and Sustainability

MuniFin kicked off its 2024 funding programme of EUR 9–10 billion with a 10-year EUR 1 billion benchmark bond on 10 January. The benchmark ended up more than two times oversubscribed, as MuniFin carved out demand in a record volume week in the market.

The orderbooks were opened on with guidance at MS+26 bps area, but MuniFin was able to tighten the guidance and the books were closed at MS +24bps and in excess of EUR 2.2 billion.

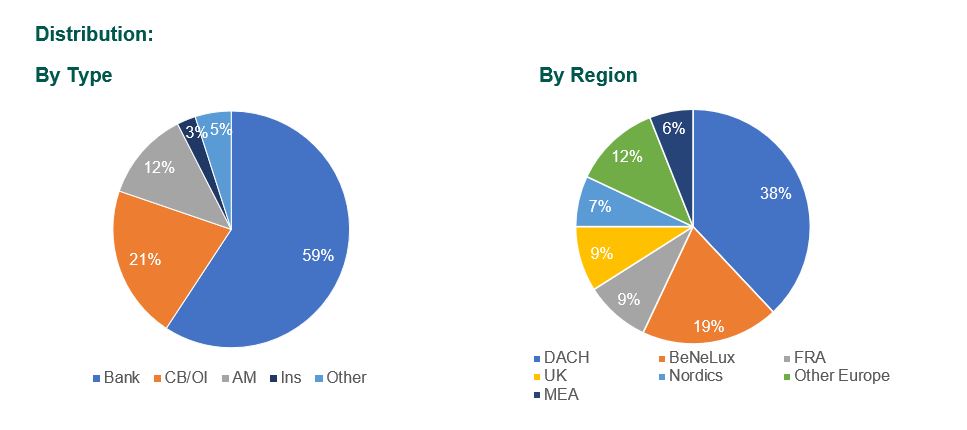

Investor demand was driven by high-quality accounts and saw a particular interest from banks, central banks and official institutions, which comprised of 80% share of allocations.

Geographically the demand was particularly high in key European regions, with the Central European countries of Germany, Austria, and Switzerland comprising 38% of the allocations and Benelux 19%.

“Our commitment to the EUR market remains strong. This was our first benchmark of the year and the first 10-year benchmark in the last two years. Despite the heavy supply, investor demand in MuniFin benchmarks remains strong. Thank you to all investors, who participated and our lead managers for a successful transaction” says Antti Kontio, Head of Funding and Sustainability at MuniFin.

MuniFin’s 2024 opening trade in an extremely competitive market is a remarkable success.

“The strategy undertaken to benefit from favourable market conditions, while differentiating from the other supply to attain price objectives, highlights the agility of the funding team to adapt in a competitive beginning of year window”, said Thomas Leocadio, Co-Head Public Sector Origination at Natixis.

“Congratulations to the MuniFin team on another great result in the EUR market issuing a well-oversubscribed 10-year benchmark at limited concession despite an extremely busy EUR primary market. Over the past years, MuniFin has established themselves as the leading Nordic SSA issuer in the EUR market and Danske Bank is proud to have supported MuniFin throughout that journey.” Gustav Landström, Head of SSA Origination, Danske Bank

“At a time of increased uncertainty around state budgets and government elections, public-sector issuers with a dedicated mandate offer attractive alternatives for investors. MuniFin today did just that with their successful 2024 opening trade that added a new line on the long end of their curve and achieved strong investor reception with a high-quality book of over EUR 2.2bn.” Patrick Seifert, Head of Primary Markets & Global Syndicate, LBBW

“Congratulations are in order for the MuniFin team that not only achieved a successful first benchmark returning to the 10-year tenor but navigated through a never-before-seen volume week in the EUR SSA primary market. The strategy undertaken to benefit from favourable market conditions, while differentiating from the other supply to attain price objectives, highlights the agility of the funding team to adapt in a competitive beginning of year window. It was a pleasure to be involved on this transaction and we look forward to the continued success of MuniFin in 2024.” Thomas Leocadio, Co-Head Public Sector Origination, Natixis

“A great result from MuniFin and its first EUR Benchmark of the year, in what has been a record-breaking week in terms of primary issuance volume. With a well oversubscribed orderbook and spread tightening of 2bps from guidance, MuniFin once again proves its excellent track record in the EUR market. SEB is delighted to have been a part of this transaction and to have supported MuniFin reaching their funding target of EUR 9-10bn for 2024.” Anna Sjulander, Head of SSA Origination at SEB

Further information

Joakim Holmström, Executive Vice President, Capital Markets and Sustainability Tel. +358 50 4443 638

Antti Kontio, Head of Funding and Sustainability Tel. +358 50 3700 285